As Associate Director at CBRE, Head of Residential Research, Craig is responsible for managing the company’s Residential Research activity in Australia, covering residential markets across the country. His role includes monitoring and interpreting market trends, data collection and database management. Outputs are directed to both internal and external clients and take the form of MarketView publications, reports, client presentations and consultancy reports.

Even ahead of last week's interest rate decision by the Reserve Bank of Australia, Australia's residential markets were already showing positive signs of improvement.

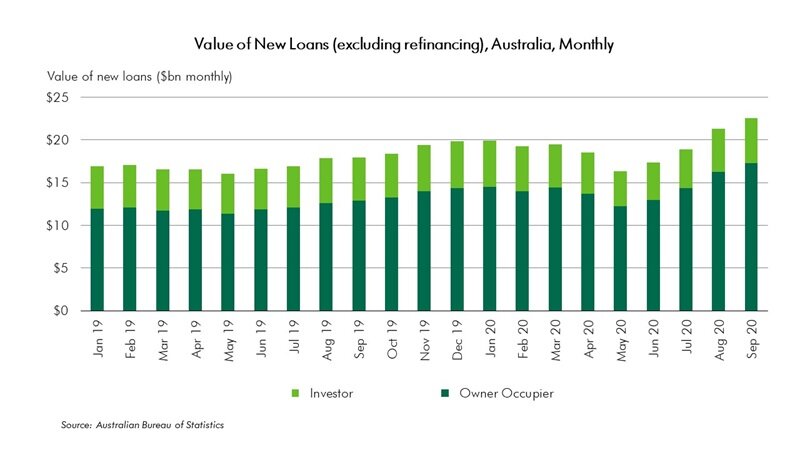

New residential finance in September, at $22.5 billion, had grown for the fourth consecutive month. In fact, the monthly total was the highest lending figure in over two years. This was driven by owner-occupiers, with the past two months recording the highest monthly owner-occupier results on record. Although slower to react, investor finance was also showing some promising signs.

The number of new owner-occupier loan commitments has risen strongly across the board (up by around 30% in the September quarter compared with June), but particularly so for the construction of dwellings (up 35%) and the purchase of land (up over 80%). This has been driven by a booming first home buyer market.

There is no doubt now that the combination of record low interest rates, federal government stimulus (HomeBuilder and the First Home Loan Deposit Scheme) and state government subsidies is proving to be exceptionally strong, despite concerns remaining with regards the jobs market heading into 2021.

The number of owner-occupier first home buyer loans over the past three months is approaching the record levels witnessed in 2009 and is likely to remain elevated until at least the end of the year, or for however long Federal government stimulus remains available.

Refinancing levels have also been high, with strong competition amongst lenders, particularly for high-quality borrowers.

These trends are largely reflected across all states.

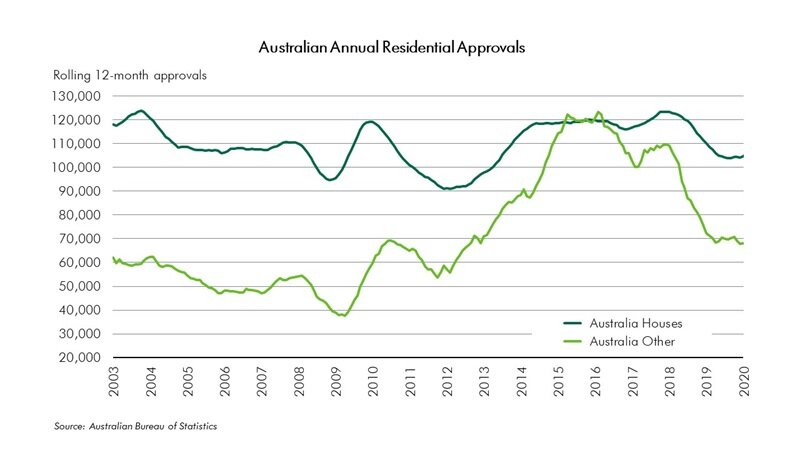

Residential building approvals were also up, with a noted jump in house approvals. At 10,466 nationally in September, the monthly total has increased for three months now, and has topped 10,000 for the first time since mid-2018. Again, these numbers should strengthen further over the remainder of 2020 at least and provide support to the residential construction industry in 2021.

Medium/high density approvals volume also rose in September, interestingly driven by higher volume in Perth and Brisbane. On an annual basis, however, medium/high density approvals volume remains at its lowest levels since 2013 and 46% below the 2016 peak. It will take a combination of sustained growth in investor demand and the reopening of international borders before a prolonged upturn can be expected.

The Reserve Bank of Australia, in their interest rate decision and subsequent statement on monetary policy, highlight that residential market conditions across the country are still uneven. Prices in Sydney and Melbourne had declined in the three months since August, but had grown in other capitals and regional locations. Vacancy rates remained elevated in Sydney and Melbourne, which was impacting rents, largely in the apartment sector. This may negatively impact returns. New listings and auction clearance rates were recovering; however, with the exception of Melbourne. That recovery will come as lockdowns ease.

Low interest rates are here to stay, and while the RBA stated they are not contemplating further reductions to the cash rate, they also do not expect to see any rises for at least three years. This provides some degree of certainty for borrowers.

The Bank did make some pertinent points that still serve a note of caution for the residential markets heading into 2021, however. These include:

that while Australia's economy has performed better than had been anticipated, the outlook for growth still involves considerable uncertainty related to the course of the pandemic, both in Australia and overseas;

recovery is expected to be extended and bumpy;

the expectation that the unemployment rate will increase in the near term as some workers return to the labour force and support such as JobKeeper tighten and then lapse. While a peak unemployment rate of a little under 8% is forecast by the end of 2020, only gradual improvement is expected, with the rate still expected to be just over 6% by the end of 2022; and

as a result, wages growth (and inflation) are expected to remain low.

The first quarter of 2021 remains the litmus test for the residential markets. This is when government support packages such as JobKeeper are slated to end, while most outstanding bank mortgage deferrals will need to be resolved. The pent-up demand that has been released as lockdown restrictions are eased will also taper.

This may still see negative pressures grow in some markets. A continuation of some forms of government stimulus may still be necessary to keep recovery on track.

Nonetheless, If the markets can work through the inevitable challenges that will come in the first half of 2021, it is likely they will have come out of the COVID-19 pandemic downturn in a much better shape than had been anticipated.

![ConstantineMimigiannis_Headshot_23012020_CC[1].png](https://images.squarespace-cdn.com/content/v1/5c197a32b105982976e5e89b/1599199935407-TQP295EY5V74S5TX6WDO/ConstantineMimigiannis_Headshot_23012020_CC%5B1%5D.png)

![TSK - no background[1].png](https://images.squarespace-cdn.com/content/v1/5c197a32b105982976e5e89b/1595989900501-M4Z3GB70TR35V89VYA5I/TSK+-+no+background%5B1%5D.png)